ॐ असतो मा सद्गमय

CBDT has clarified that the process for cancellation of registration is to be initiated strictly in accordance with section 12AA(3) and 12AA(4) after carefully examining the applicability of these provisions. CBDT has also cautioned that since cancellation of registration of trust shall invite accereted income tax as per Finance Act 2016, authorities are, therefore, advised not to cancel the registration of a charitable institution granted u/s 12AA just because the proviso to section 2(15) comes into play. CBDT has sternly forbidden to cancel registration merely on the ground that the cut-off specified in the proviso to section 2(15) of the Act is exceeded in a particular year without there being any change in the nature of activities of the institution [Circular 21/2016, Dated: May 27, 2016]

TCS provisions have been made applicable to all the goods and services wef 01-06-2016. While the provisions are intended to frame a system of reporting high value transactions to curb black money, the law framed by the parliament in this regard is plagued by number of doubts and issues which can clog the very implementation of provisions. The author has made a humble attempt to consolidate the issues involved in this taxation as under:

Relevant TCS provisions

As per Section 206C(1D) amended wef 01-06-2016,

Every person, being a seller, who receives any amount in cash as consideration for sale of bullion or jewellery or any other goods (other than bullion or jewellery or providing any service, shall, at the time of receipt of such amount in cash, collect from the buyer, a sum equal to one per cent of sale consideration as income-tax, if such consideration,—

(i) for bullion, exceeds two hundred thousand rupees; or

(ii) for jewellery, exceeds five hundred thousand rupees;or

(iii) for any goods, other than those referred to in clauses (i) and (ii), or any service, exceeds two hundred thousand rupees

Provided that no tax shall be collected at source under this sub-section on any amount on which tax has been deducted by the payer under Chapter XVII-B

(1E) Nothing contained in sub-section (1D) in relation to sale of any goods (other than bullion or jewellery) or providing any service shall apply to such class of buyers who fulfil such conditions, as may be prescribed

Explanation.—For the purposes of this section-

(aa) buyer” with respect to—

(i) sub-section (1) means a person who obtains in any sale, by way of auction, tender or any other mode, goods of the nature specified in the Table in sub-section (1) or the right to receive any such goods but does not include,—

(A) a public sector company, the Central Government, a State Government, and an embassy, a High Commission, legation, commission, consulate and the trade representation, of a foreign State and a club; or

(B) a buyer in the retail sale of such goods purchased by him for personal consumption;

(ii) sub-section (1D) or sub-section (1F) means a person who obtains in any sale, goods of the nature specified in the said sub-section;

(c ) seller” means the Central Government, a State Government or any local authority or corporation or authority established by or under a Central, State or Provincial Act, or any company or firm or co-operative society and also includes an individual or a Hindu undivided family whose total sales, gross receipts or turnover from the business or profession carried on by him exceed the monetary limits specified under clause (a) or clause (b) of section 44AB during the financial year immediately preceding the financial year in which the goods of the nature specified in the Table in sub-section (1) or sub-section (1D)] are sold or services referred to in sub-section (1D) are provided

Analysis

Persons who are required to collect TCS as “Seller” are:

Persons not covered:

Scope of Transactions Covered

As per S.206C(ID) TCS is applicable to Seller who receives any amount in cash as consideration for :

Issues Involved:

The Principal issue involved is whether TCS is to be collected on:

Opinion:

Finance Minister’s Budget Speech (para 149 of the Budget Speech)

Memorandum Explaining the provisions of Finance Bill 2016

The existing provision of section 206C of the Act, inter alia, provides that the seller shall collect tax at source at specified rate from the buyer at the time of sale of specified items such as alcoholic liquor for human consumption, tendu leaves, scrap, mineral being coal or lignite or iron ore, bullion etc. in cash exceeding two lakh rupees.

In order to reduce the quantum of cash transaction in sale of any goods and services and for curbing the flow of unaccounted money in the trading system and to bring high value transactions within the tax net, it is proposed to amend the aforesaid section to provide that the seller shall collect the tax at the rate of one per cent from the purchaser on sale of motor vehicle of the value exceeding ten lakh rupees and sale in cash of any goods (other than bullion and jewellery), or providing of any services (other than payments on which tax is deducted at source under Chapter XVII-B) exceeding two lakh rupees.

It is also proposed to provide that the sub-section (1D) relating to TCS in relation to sale of any goods (other than bullion and jewellery) or services shall not apply to certain class of buyers who fulfil such conditions as may be prescribed.

This amendment will take effect from 1st June, 2016.

Section 206C(1D)

Every person, being a seller, who receives any amount in cash as consideration for sale of bullion or jewellery or any other goods (other than bullion or jewellery or providing any service, shall, at the time of receipt of such amount in cash, collect from the buyer, a sum equal to one per cent of sale consideration

Hence

So, there appears to be a contradiction with in the provisions of law and memorandum explaining provisions of finance bill. While as per Memorandum explaining finance bill and FM’s Speech, TCS is applicable only on cash sale of goods for sum exceeding Rs. 2 lacs, the express provisions provide that even if a paltry amount against sale exceeding Rs. 2 lacs is received in cash, the entire sale consideration to be brought under TCS net and not to be restrained to the amount of cash receipt.

The point of taxation for TCS on sale of goods or provision of service is

“the time of receipt of such amount in cash” and not Sale of Goods

Hence ,If sale consideration amount is outstanding on 31-05-2016, and any amount is received there after in cash , the assessee is liable to pay tax on the amout recived after 31-05-2016 in respect of transactions executed before 31-05-2016. However, another incidental issue involved is :

Opinion

As per Section 206C(ID):

“Every person, being a seller, who receives any amount in cash as consideration for sale of bullion or jewellery or any other goods (other than bullion or jewellery or providing any service, shall, at the time of receipt of such amount in cash, collect from the buyer, a sum equal to one per cent of sale consideration as income-tax”

TCS to be collected on 1% of sale consideration and not amount in cash as consideration for sale of goods. Hence, TCS might apply on entire sum reducing the amount received before 01-06-2016.

As per Section 206C(ID), TCS is applicable on sale of goods orprovision of service. However, where both sale of goods andprovision of service is involved, an issue arises that whether TCS provisions u/s 206C(ID) shall become applicable.

Opinion

As per Article 366(29A), transfer of property in goods in case of works contract is deemed as sale. Further as per Section 66E(b) and 66E(h), service portion is declared service in case of works contract. Hence TCS shall become applicable to works contract also. However the matter needs clarification by legislature.

4 Whether 1% TCS to be collected on the amount of Vat and Excise Duty Charged.

Opinion

The word sale consideration is not defined under Income Tax Law but as per Section 145A,

“…….the valuation of purchase and sale of goods and inventory for the purposes of determining the income chargeable under the head “Profits and gains of business or profession” shall be adjusted to include the amount of any tax, duty, cess or fee (by whatever name called) actually paid or incurred by the assessee to bring the goods to the place of its location and condition as on the date of valuation

………..”

Hence TCS to be charged on full amount of sale consideration. Taxes, Duties, Cess or fee can not be segregated. The word “Sale Consideration” can not be equated with “Gross Turnover” u/s 44AB , where in refundable taxes are required to be excluded.

The Definition of buyer under Explanation to Section 206C, specifically includes “right to receive” for the purposes of 206C(1), however for 206C(1D), it is missing. So, when advance is paid by the buyer towards right to receive the goods, whether TCS provisions can be applied

Opinion:

The matter requires clarification. If such a version is adopted, the assesses might resort to the policy of receiving entire sum as advance in cash. There by defeating the purpose of introducing the provisions.

Opinion: Since TCS is applicable only to receipt of cash as consideration for sale, TCS provisions u/s 206C(1D) shall not apply where payment is received through bearer cheque

Opinion: Since TCS is applicable only to receipt of cash as consideration for sale, TCS provisions u/s 206C(1D) shall not apply where payment is received through exchange of goods.

As per Section 206C(1) for alcoholic liquor for human consumption, tendu leaves, timber, forest products, scrap, coal, lignite or iron ore,

and as per S.206C(1C), for parking lot, toll plaza and mining and quarrying, TCS is applicable at the time of debit of amount to the account of buyer or receipt of amount in cash or cheque or draft or any other mode, which ever is earlier.

At the same time 206C(1D) is applicable to receipt of any amount in cash as consideration for sale of goods or provision of service.

The issue that arises is that whether 206C(ID) can result in Duplication of levy in respect of goods or services covered by other provisions.

Opinion

One may follow the Latin Maxim Generalia Specialibus Non Derogant i.e. the provisions of a general statute must yield to those of a special one. But the matter should have been clarified by the legislature instead of leaving the taxpayer to the mercy of tax officials.

Opinion: Section 206C does not put any embargo upon transactions with non residents.

But in case of import of goods, where seller is non resident, the provisions of the Act can not be extended beyond India. Further, it the seller who is liable to collect tax and not the resident buyer.

In case of export of goods, where buyer is non resident, enforcing deposit of tax on behalf of buyer who has no income chargeable to tax in India can not be sustained in the Court of law, because TCS is tax collected and paid on behalf of buyer. Further as per Section 9, where operations of non resident are confined to procurement of goods in India, no Income can be deemed to have accrued or arisen in India.

Opinion

High Sea Sales take place before the goods cross the Custom Frontiers of India. Although the Income Tax Act does not extend beyond India and the word “India” is defined u/s 2(25A) as India” means the territory of India as referred to in article 1 of the Constitution, its territorial waters, seabed and subsoil underlying such waters, continental shelf, exclusive economic zone or any other maritime zone as referred to in the Territorial Waters, Continental Shelf, Exclusive Economic Zone and other Maritime Zones Act, 1976 (80 of 1976), and the air space above its territory and territorial waters

However Section 206C(ID) does not place any embargo upon such transactions and hence shall be covered by TCS

Conclusion: Section 206C(ID) as introduced by Finance Act 2016 and to be implemented from 01-06-2016 requires clarification on number of issues discussed here in above. The better sense of wisdom demands that issues which can pest the large number of tax payers be resolved before launching the avalanche of enigma.

Finance Bill 2016 comprised 12 Chapters, 238 Clauses and 15 Schedules spread over 221 pages. It brought in Krishi Kalyan Cess, Infrastructure Cess, Equalization Levy, The Income Declaration Scheme, Direct and Indirect Tax Dispute Resolution Schemes and amendments previous Finance Acts ranging from Finance Act 2001 to 2015 . The Journey of Change did not end here and In Lok Sabha 47 further amendments were brought in Finance Bill on 29-04-2016 including insertion of 3 more clauses there by increasing total clauses to 241.

Out of this first 115 clauses, Introduction of Equalization Levy under

Chapter VIII, The Income Declaration Scheme under Chapter IX and Direct Tax Dispute Resolution Scheme under Chapter X and Schedule I on tax rates deal with the Changes made in Direct Taxes.

For AY 2017-18, In case of domestic companies where its total turnover or the gross receipt in the previous year 2014-15 does not exceed five crore rupees tax shall be charged @ 29%.

Comments:

Tax rate for financial year 2016-17 has been determined on the basis of FY year 2014-15, because companies have already filed their return for 2014-15. Hence so that companies may not under state their turnover for 2016-17, to avail 1% tax benefit, the base year of 2014-15 instead of 2015-16 has been taken. At the same time if turnover of the company for 2014-15 is merely 50 lacs and turnover for 2015-16 is 500 crores, still rate of 29% shall apply for AY 2017-18

In case of companies not in existence in 2014-15, whether turnover can be assumed lesser than 5 crore is a moot point not answered in Finance Act.

Brief Discussion on Schemes

As per Soverign Gold Bonds Scheme, physical form of gold is converted into form of Soveriegn Gold Bonds (SGB). Investors are assured of market value of gold at the time of maturity plus periodical interest @ 2.75% payable semi annually. The tenure of bonds is 8 years with exit option at 5th , 6thand 7th year. Bonds can be used as collaterals for loan[Loan to value (LTV) to be decided by RBI. Bonds can also be traded on exchange thus providing an option to make early exit. Bonds carry soverign guarantee against capital invested and interest. Only resident Individuals, HUFs, trusts, universities and charitable institutions are eligible to invest. Joint holding in Gold Bonds is allowed and minors can also hold the bonds provided application is made by guardian of the minor. Bonds are issued in denomination of gram and and minimum investment in SGB is 2 gms and maximum investment in a financial year is 500 gms. The issue price of SGB is previous week (Mon-Friday) simple average of closing price of gold of 999 purity published by Indian Bullion and Jewellers Association Ltd. (IBJA). The redemption price is also similarly worked out. In case of joint holding limit applies to first holder. The bonds are sold through banks, stock holding corporation and designated post offices and their commission is 1% of subscription amountand receiving offices shall share at least 50% of the commission so received with the agents or sub agents for the business procured through them.

Tax Benefits Imparted for Gold Monetization and Gold Bond Schemes

Comments : Interest on Gold Bond Scheme has not been exempted. Also redemption under gold bonds scheme has been exempted, however, transfer has not been exempted. However transfer has been imparted indexation benefit.

Clause 2(23C) inserted to provide that “hearing” includes communication of data and documents through electronic mode

As per Section 282A inserted by the Finance Act, 2008, w.e.f. 1-6-2008.

On Authentication of notices and other documents.

282A. (1) Where this Act requires a notice or other document to be issuedby any income-tax authority, such notice or other document shall be signed in manuscript by that authority.

(2) Every notice or other document to be issued, served or given for the purposes of this Act by any income-tax authority, shall be deemed to be authenticated if the name and office of a designated income-tax authority is printed, stamped or otherwise written thereon.

(3) For the purposes of this section, a designated income-tax authority shall mean any income-tax authority authorised by the Board to issue, serve or give such notice or other document after authentication in the manner as provided in sub-section (2)

Section 282A(1) has been amended wef 01-06-2016 to provide that Where this Act requires a notice or other document to be issued by any income-tax authority, such notice or other document shall be signed in manuscript by that authority signed and by that authority in accordance with such procedure as may be prescribed

Comments: While section 282A(1) deals with manner of issuing documents by Income Tax Authority , Section 282 deals with stage subsequent to issuing of documents i.e. manner of service of a notice or summon or requisition or order or any other communication under this Act. Section 282 requires delivery or transmission by post or approved Courier or in the manner provided in Code of Civil Procedure or in form of electronic record under Information Technology Act, to an address as specified in Rule 127 [ R.127 inserted w.e.f. 02-12-2015] in order to effectuate service under the law.

The Finance Act, 2015 had amended the definition of income under clause (24) of section 2 of the Act so as to provide that the income shall include assistance in the form of a subsidy or grant or cash incentive or duty drawback or waiver or concession or reimbursement (by whatever name called) by the Central Government or a State Government or any authority or body or agency in cash or kind to the assessee other than the subsidy or grant or reimbursement which is taken into account for determination of the actual cost of the asset in accordance with the provisions of Explanation 10 to clause (1) of section 43 of the Income-tax Act.

As a result grant or cash assistance or subsidy etc. provided by the Central Government for budgetary support of a trust or any other entity formed specifically for operational zing certain government schemes will be taxed in the hands of trust or any other entity. Therefore, it is proposed to amend section 2(24) to provide that subsidy or grant by the Central Governmentfor the purpose of the corpus of a trust or institution established by the Central Government or State government shall not form part of income.

Provisions of section 6(3) earlier amended by Finance Act 2015 and reiterated in Finance Bill 2016

| A company is said to be resident in India in any previous year, if,— |

| (i) | it is an Indian company; or | |

| (ii) | its place of effective management, in that year, is in India. |

| Explanation.—For the purposes of this clause “place of effective management” means a place where key management and commercial decisions that are necessary for the conduct of the business of an entity as a whole are, in substance made. |

The amended provisions of Section 6(3) were to come into effect from Assessment Year 2016-17. The Finance Bill, 2016 proposes to defer the implementation of POEM as test of residency by one year to apply from Assessment Year 2017-18 onwards. The Finance Minister in his speech stated that “The determination of residency of foreign company on the basis of Place of Effective Management (POEM) is proposed to be deferred by one year.”

This is to be achieved by omitting clause (ii) of Section 4 of

the Finance Act 2015 with effect from 1-4-2016. The amendment to Finance Act 2015 is to be carried out vide Part XV of the Finance Bill 2016. Thus, for assessment year 2016-17, the test of residency for foreign companies continues to be on the touch stone of “control and management’’ of its affairs

In the context of implementation of POEM based residence

rule, certain issues, relating to the applicability of current provisions of the Act to a company which is incorporated outside India and has not earlier been assessed to tax in India, have arisen. In particular, the issues relate to applicability of specific provisions of the Act relating to Advance tax payment, applicability of TDS provisions, computation of total income, set off of losses and manner of application of transfer pricing regime. These provisions have compliance requirements which would not have been undertaken by the company at relevant time due to absence of any such requirement under tax laws of country of incorporation of such company. Similarly, issues of computation of depreciation also arise when in earlier years it has not been subject to computation under the Act.

Problems highlighted also arise due to the fact that a

company may be claiming to be a foreign company not resident in India but in the course of assessment, it is held to be resident based on POEM being in fact in India. This determination would be well after closure of the previous year and it may not be possible for company to undertake many of procedural requirements. Representations have also been made by stakeholders that the implementation of POEM be deferred by a year, by which time clarity regarding guidelines and applicability of other provisions of the Act would be in place

Chapter XII-BC introduced in Income Tax Act 1961

115JH(1) Where a foreign company is said to be resident in India in any previous year and such foreign company has not been resident in India in any of the previous years preceding the said previous year, then, notwithstanding anything contained in this Act and subject to the conditions as may be notified by the Central Government in this behalf, the provisions of this Act relating to the computation of total income, treatment of unabsorbed depreciation, set off or carry forward and set off of losses, collection and recovery and special provisions relating to avoidance of taxshall apply with such exceptions, modifications and adaptations as may be specified in that notification for the said previous year:

Provided that where the determination regarding foreign company to be resident in India has been made in the assessment proceedings relevant to any previous year, then, the provisions of this sub-section shall also apply in respect of any other previous year, succeeding such previous year, if the foreign company is resident in India in that previous year and the previous year ends on or before the date on which such assessment proceeding is completed.

(2) Where, in a previous year, any benefit, exemption or relief has been claimed and granted to the foreign company in accordance with the provisions of sub-section (1), and, subsequently, there is failure to comply with any of the conditions specified in the notification issued under sub-section (1), then,—

(i) such benefit, exemption or relief shall be deemed to have been wrongly allowed;

(ii) the Assessing Officer may, notwithstanding anything contained in this Act, re-compute the total income of the assessee for the said previous year and make the necessary amendment as if the exceptions, modifications and adaptations referred to in sub-section (1) did not apply; and

(iii) the provisions of section 154 shall, so far as may be, apply thereto and the period of four years specified in sub-section (7) of that section being reckoned from the end of the previous year in which the failure to comply with the condition referred to in sub-section (1) takes place.

(3) Every notification issued under this section shall be laid before each House of Parliament.

Comments

For Example during assessment for AY 2017-18 completed on 24-12-2020, it comes to notice of AO that POEM of foreign company is in India. So, exceptions u/s 115JH shall not only apply to PY 17-18,18-19 also i.e. relevant to AY 18-19 and AY 19-20 But not w.r.t. AY 2020-21 relevant to previous year 2019-20.

However other assesses are not provided any relief from procedural requirement for ignorance about their tax liability.

A “Special Notified Zone” (SNZ) had been created to facilitate shifting of operations by foreign mining companies (FMC) to India and to permit the trading of rough diamonds in India by the leading diamond mining companies of the world. The activity of FMC of mere display of rough diamonds even with no actual sale taking place in India may lead to creation of business connection in India of the FMC. This potential tax exposure has been an area of concern for the mining companies willing to undertake these activities in India. In order to facilitate the FMCs to undertake activity of display of uncut diamond (without any sorting or sale) in the special notified zone, it is proposed to amend section 9 of the Act wef AY 2016-17 by inserting clause (e) in Expl 1 to S.9(i) as under:

“ In the case of a foreign company engaged in the business of mining of diamonds, no income shall be deemed to accrue or arise in India to it through or from the activities which are confined to the display of uncut and unassorted diamond in any special zone notified by the Central Government in the Official Gazette in this behalf”

In Finance Act 2015, section 9A was inserted in backdrop of the fact thatunder the existing provisions, the presence of a fund manager in India may create sufficient nexus of the off-shore fund with India and may constitute a business connection in India even though the fund manager may be an independent person. Also due to nexus with India, activity in respect of investments outside India for an off-shore fund, the profits made by the fund from such investments may be liable to tax in India . Section 9A was inserted to promote promotion of off shore funds in India subject to fulfilment of certain conditions

Howeverconditions u/s 9A(3)(k) that the fund shall not carry on or

control and manage, directly or indirectly, any business in India or from India is being modified to state that the fund shall not carry on or control and manage, directly or indirectly, any business in India. The condition of not carrying on or controlling and managing business from India abolished

One of the other conditions is that fund must be resident of country with which DTAA or TIEA subsists. However in case of some off shore funds like large pension funds or mutual funds from USA or SICAVs (open ended collective investment schemes) from Luxembourg are not resident as per tax laws of other country but still information may be gathered about these as DTAA and TIEA also applies to persons not resident as per tax laws of that country. Hence condition u/s 9A(3)(b) being amended to cover the off shore funds incorporated outside India which are covered by DTAA or TIEA.

Internet advertising is rapidly growing both in terms of revenue and share in the total advertising market. The volume of internet advertising reached USD 135.4 billion in 2014. The market for internet advertising is projected to grow at a rate of 12.1% per year during the period 2014 to 2019. As the stakes started rocketing, taxing such virtual transactions attained prominence. The existing provisions of the income-tax statute were unable to tie the noose around these transactions. Perhaps the reason is Indian income-tax legislation is still governed physical presence test. Hence the concept of Equalization levy introduced.

Equalization Levy:

Ø Applicable from date to be notified by Central Government

Ø It extends to whole of India except the state of J&K

Ø Introduced vide Chapter VIII of Finance Bill 2016. Vide S. 160 to S.177 of Finance Bill 2016

Ø Rate @6% as per S.162(1) of Finance Bill

Ø Services covered by Equalization Levy:

Ø Charge of tax is on amount of consideration received or receivable by Non Resident from:

(i) a person resident in India and carrying on business or profession; or

(ii) a non-resident having a permanent establishment in India.

Ø Amount chargeable to equalization levy has been exempted u/s 10(50).

Ø Equalization levy shall not apply where

Ø Equalization Levy shall operate like TDS and shall be deducted from payment to non resident and to be deposited by 7th of following calendar month [Word calendar month specifically mentioned . Hence whether Arvind Mills (Karnatka High Court ) shall apply for other provisions and lunar month shall apply ?] [S. 163]

Ø 1% Interest for delayed payment u/s 167.

Ø Even if equalization levy not deducted, it shall be deposited by service recipient out of his own pocket. S. 163(3) [Whether on gross basis ?]

Ø Disallowance u/s 40(a)(ib) shall be attracted for failure to deduct levy or deposit after deducting till due date of return on amount paid or payable to non resident. [Here words “paid” also used to resolve the controversy of Merilyn Shipping]. Allowance of expenditure only in the year of deposit. [S. 163(3) situation not dealt here where amount deposited without deducting]

Ø Statements to be filed with in prescribed time after end of financial year. Belated/Rectified statements may be filed with in 2 years from end of financial year [Here no requirement to file revised return only if original filed in time]. AO may also give notice to file the return. [S.164] Penalty for belated return @ Rs. 100/- per day u/s 169

Ø Intimation and processing of intimation with in one year from the end of financial year in which statement is filed. [However u/s 143(1) it is one year from the end of assessment year.]

Ø Rectification of intimation by AO/assessee with in one year from end of financial year in which intimation issued.[Not served]S.166

Ø Penalty for failure to deduct = Equal to equalization levy [Even if paid u/s 163(3) out of own pocket ?]

Ø Penalty for failure to deposit= Rs. 1000/- per day Max. Equalization levy.

Ø Penalty is subject to pleading reasonable cause and after providing opportunity of being heard[S. 170]

Ø Appeal to CIT A u/s 171; ITAT u/s 172; Prosecution for false statement u/s 173; Applicability of certain provisions regarding summons u/s 131; survey u/s 133A etc

Ø Rule making power is u/s 176 and power to remove difficulties u/s 177

Constitutonal Validity of Equalization levy:

As per S. 161(d) equalization levy means tax leviable on consideration received or receivable for any specified service under the provisions of this Chapter.

The word “tax” has not been defined in Chapter VIII of Finace Bill 2016. As per Clause (j) to Section 161 provides that words or expressions used but not defined in the said Chapter and which are specifically defined in the Income-tax Act; shall have the meanings respectively assigned to them in the Income-tax Act. Section 2(43) of the Income-tax Act defines tax as under:

“”Tax” in relation to the assessment year commencing on the 1st day of April, 1965, and any subsequent assessment year means income-tax chargeable under the provisions of this Act, and in relation to any other assessment year income-tax and super-tax chargeable under the provisions of this Act prior to the aforesaid date and in relation to the assessment year commencing on the 1st day of April, 2006, and any subsequent assessment year includes the fringe benefit tax payable under Section 115WA”

Accordingly, the term ‘tax’ in Chapter VIII of the Finance Bill should mean ‘income-tax’.

Also in order to avoid double taxation of income tax equalization levy has been exempted u/s 10(50). Further if equalization levy had not been tax on income it would have found place in section 43B like other taxes and not 40(a)(ib).

The legislative intention of the proposed Equalisation Levy can be gathered from the budget speech of the Hon’ble Finance Minister (while presenting Finance Bill 2016). At para 151 of his speech he said:

“151. In order to tap tax on income accruing to foreign e-commerce companies from India, it is proposed that a person making payment to a non-resident, who does not have a permanent establishment, exceeding in aggregate ` 1 lakh in a year, as consideration for online advertisement, will withhold tax at 6% of gross amount paid, as Equalisation Levy. The Levy will only apply to B2B transactions.

The Mumbai Tribunal in the case of ADIT v. Chiron Behring GmbH & Co (2008) 24 SOT 278 (Mum) had an occasion to examine the applicability of India-Germany Double Taxation Avoidance Agreement. In the said case, the assessee was liable to pay ‘trade tax’ under the German domestic tax provisions. The Revenue authorities argued that such tax is not covered within the tax treaty. The Mumbai Tribunal rejected this argument by observing that Article 6 of the German Trade Tax Act states ‘The basis of taxation for Trade Tax is the income from the business’. From this finding, it concluded that the trade tax is not a turnover tax, but only is tax on the income from business. Such tax was thus held to be eligible for tax treaty purposes.

Hence equalization levy is a tax on income.

includes dividends of a domestic company > Rs. 10,00,000, then amount exceeding Rs 10 lacs shall be chargeable to tax @10% .

An amendment has been made in Finance Act 2016 as passed by Loksabha providing that for the purpose of calculating limit of 10 lacs income in aggregate by way of dividends to be taken and 10% tax to be computed on aggregate amount of dividends in excess of 10 lacs. Thus individual dividends of domestic company can not be segregated to apply the tax u/s 115BBDA.

Persons not covered:

iii) The legislature realized the anomaly and Motor Vehicle for value exceeding Rs. 10 lacs were planted to specifically enacted Sub-section 206C(1F). As per Section 206C(1F)

Every person, being a seller, who receives any amount as consideration for sale of a motor vehicle of the value exceeding ten lakh rupees, shall, at the time of receipt of such amount, collect from the buyer, a sum equal to one per cent of the sale consideration as income-tax.

The definition of buyer also extended to include the person who obtains in any sale, goods of the nature specified in the said sub-section (i.e. Motor Vehicle for value exceeding Rs. 10 lacs)

Comments :

Relevant TCS provisions

As per Section 206C(1D) amended wef 01-06-2016,

Every person, being a seller, who receives any amount in cash as consideration for sale of bullion or jewellery or any other goods (other than bullion or jewellery or providing any service, shall, at the time of receipt of such amount in cash, collect from the buyer, a sum equal to one per cent of sale consideration as income-tax, if such consideration,—

(i) for bullion, exceeds two hundred thousand rupees; or

(ii) for jewellery, exceeds five hundred thousand rupees;or

(iii) for any goods, other than those referred to in clauses (i) and (ii), or any service, exceeds two hundred thousand rupees

Provided that no tax shall be collected at source under this sub-section on any amount on which tax has been deducted by the payer under Chapter XVII-B

(1E) Nothing contained in sub-section (1D) in relation to sale of any goods (other than bullion or jewellery) or providing any service shall apply to such class of buyers who fulfil such conditions, as may be prescribed

Explanation.—For the purposes of this section-

(aa) buyer” with respect to—

(i) sub-section (1) means a person who obtains in any sale, by way of auction, tender or any other mode, goods of the nature specified in the Table in sub-section (1) or the right to receive any such goods but does not include,—

(A) a public sector company, the Central Government, a State Government, and an embassy, a High Commission, legation, commission, consulate and the trade representation, of a foreign State and a club; or

(B) a buyer in the retail sale of such goods purchased by him for personal consumption;

(ii) sub-section (1D) or sub-section (1F) means a person who obtains in any sale, goods of the nature specified in the said sub-section;

(c ) seller” means the Central Government, a State Government or any local authority or corporation or authority established by or under a Central, State or Provincial Act, or any company or firm or co-operative society and also includes an individual or a Hindu undivided family whose total sales, gross receipts or turnover from the business or profession carried on by him exceed the monetary limits specified under clause (a) or clause (b) of section 44AB during the financial year immediately preceding the financial year in which the goods of the nature specified in the Table in sub-section (1) or sub-section (1D)] are sold or services referred to in sub-section (1D) are provided

Analysis

Scope of Transactions Covered

As per S.206C(ID) TCS is applicable to Seller who receives any amount in cash as consideration for :

Issues Involved:

The Principal issue involved is whether TCS is to be collected on:

Opinion:

Finance Minister’s Budget Speech (para 149 of the Budget Speech)

Memorandum Explaining the provisions of Finance Bill 2016

The existing provision of section 206C of the Act, inter alia, provides that the seller shall collect tax at source at specified rate from the buyer at the time of sale of specified items such as alcoholic liquor for human consumption, tendu leaves, scrap, mineral being coal or lignite or iron ore, bullion etc. in cash exceeding two lakh rupees.

In order to reduce the quantum of cash transaction in sale of any goods and services and for curbing the flow of unaccounted money in the trading system and to bring high value transactions within the tax net, it is proposed to amend the aforesaid section to provide that the seller shall collect the tax at the rate of one per cent from the purchaser on sale of motor vehicle of the value exceeding ten lakh rupees and sale in cash of any goods (other than bullion and jewellery), or providing of any services (other than payments on which tax is deducted at source under Chapter XVII-B) exceeding two lakh rupees.

It is also proposed to provide that the sub-section (1D) relating to TCS in relation to sale of any goods (other than bullion and jewellery) or services shall not apply to certain class of buyers who fulfil such conditions as may be prescribed.

This amendment will take effect from 1st June, 2016.

Section 206C(1D)

Every person, being a seller, who receives any amount in cash as consideration for sale of bullion or jewellery or any other goods (other than bullion or jewellery or providing any service, shall, at the time of receipt of such amount in cash, collect from the buyer, a sum equal to one per cent of sale consideration

Hence

So, there appears to be a contradiction with in the provisions of law and memorandum explaining provisions of finance bill. While as per Memorandum explaining finance bill and FM’s Speech, TCS is applicable only on cash sale of goods for sum exceeding Rs. 2 lacs, the express provisions provide that even if a paltry amount against sale exceeding Rs. 2 lacs is received in cash, the entire sale consideration to be brought under TCS net and not to be restrained to the amount of cash receipt.

The point of taxation for TCS on sale of goods or provision of service is

“the time of receipt of such amount in cash” and not Sale of Goods

Hence ,If sale consideration amount is outstanding on 31-05-2016, and any amount is received there after in cash , the assessee is liable to pay tax on the amout recived after 31-05-2016 in respect of transactions executed before 31-05-2016. However, another incidental issue involved is :

Opinion

As per Section 206C(ID):

“Every person, being a seller, who receives any amount in cash as consideration for sale of bullion or jewellery or any other goods (other than bullion or jewellery or providing any service, shall, at the time of receipt of such amount in cash, collect from the buyer, a sum equal to one per cent of sale consideration as income-tax”

TCS to be collected on 1% of sale consideration and not amount in cash as consideration for sale of goods. Hence, TCS might apply on entire sum reducing the amount received before 01-06-2016.

iii) Whether TCS is applicable where both sale of goods andprovision of service is involved i.e. in the case of works contract

As per Section 206C(ID), TCS is applicable on sale of goods orprovision of service. However, where both sale of goods andprovision of service is involved, an issue arises that whether TCS provisions u/s 206C(ID) shall become applicable.

Opinion

As per Article 366(29A), transfer of property in goods in case of works contract is deemed as sale. Further as per Section 66E(b) and 66E(h), service portion is declared service in case of works contract. Hence TCS shall become applicable to works contract also. However the matter needs clarification by legislature.

Opinion

The word sale consideration is not defined under Income Tax Law but as per Section 145A,

“…….the valuation of purchase and sale of goods and inventory for the purposes of determining the income chargeable under the head “Profits and gains of business or profession” shall be adjusted to include the amount of any tax, duty, cess or fee (by whatever name called) actually paid or incurred by the assessee to bring the goods to the place of its location and condition as on the date of valuation

………..”

Hence TCS to be charged on full amount of sale consideration. Taxes, Duties, Cess or fee can not be segregated. The word “Sale Consideration” can not be equated with “Gross Turnover” u/s 44AB , where in refundable taxes are required to be excluded.

The Definition of buyer under Explanation to Section 206C, specifically includes “right to receive” for the purposes of 206C(1), however for 206C(1D), it is missing. So, when advance is paid by the buyer towards right to receive the goods, whether TCS provisions can be applied

Opinion:

The matter requires clarification. If such a version is adopted, the assesses might resort to the policy of receiving entire sum as advance in cash. There by defeating the purpose of introducing the provisions.

Opinion: Since TCS is applicable only to receipt of cash as consideration for sale, TCS provisions u/s 206C(1D) shall not apply where payment is received through bearer cheque

vii) Whether TCS is applicable where goods are exchanged under Barter System [say Jewellery is exchanged for bullion]

Opinion: Since TCS is applicable only to receipt of cash as consideration for sale, TCS provisions u/s 206C(1D) shall not apply where payment is received through exchange of goods.

viii) Whether TCS provisions under section 206C(1D) also cover the goods or services covered by other provisions.

As per Section 206C(1) for alcoholic liquor for human consumption, tendu leaves, timber, forest products, scrap, coal, lignite or iron ore,

and as per S.206C(1C), for parking lot, toll plaza and mining and quarrying, TCS is applicable at the time of debit of amount to the account of buyer or receipt of amount in cash or cheque or draft or any other mode, which ever is earlier.

At the same time 206C(1D) is applicable to receipt of any amount in cash as consideration for sale of goods or provision of service.

The issue that arises is that whether 206C(ID) can result in Duplication of levy in respect of goods or services covered by other provisions.

Opinion

One may follow the Latin Maxim Generalia Specialibus Non Derogant i.e. the provisions of a general statute must yield to those of a special one. But the matter should have been clarified by the legislature instead of leaving the taxpayer to the mercy of tax officials.

Opinion: Section 206C does not put any embargo upon transactions with non residents.

But in case of import of goods, where seller is non resident, the provisions of the Act can not be extended beyond India. Further, it the seller who is liable to collect tax and not the resident buyer.

In case of export of goods, where buyer is non resident, enforcing deposit of tax on behalf of buyer who has no income chargeable to tax in India can not be sustained in the Court of law, because TCS is tax collected and paid on behalf of buyer. Further as per Section 9, where operations of non resident are confined to procurement of goods in India, no Income can be deemed to have accrued or arisen in India.

Opinion

High Sea Sales take place before the goods cross the Custom Frontiers of India. Although the Income Tax Act does not extend beyond India and the word “India” is defined u/s 2(25A) as

India” means the territory of India as referred to in article 1 of the Constitution, its territorial waters, seabed and subsoil underlying such waters, continental shelf, exclusive economic zone or any other maritime zone as referred to in the Territorial Waters, Continental Shelf, Exclusive Economic Zone and other Maritime Zones Act, 1976 (80 of 1976), and the air space above its territory and territorial waters

However Section 206C(ID) does not place any embargo upon such transactions and hence shall be covered by TCS

iii) Litigation may arise because of services not defined under Income Tax law. In case of rent and interest, although TDS is applicable but where tax is not deducted and TCS is also not collected, the authorities might allege that rent is declared service u/s 66E of Service Tax law and interest is in form of financial services.

xii) Personal Consumption

There is no exemption for payment of TCS in respect of goods or services for personal consumption like S.206C(1)

iii) Date of merger with trust not registered u/s 12AA or not having similar objects

Further as per S.115TD(3), a trust or an institution shall be deemed to have been converted into any form not eligible for registration under section 12AA in a previous year, if,—

(i) the registration granted to it under section 12AA has beencancelled. Accereted Income tax to be paid with in 14 days from date on which order of cancellation of registration is received [as per 115TD(5)(i)].

However 115TD(5)(i) was amended by the Parliament in Loksabha to extend the period of payment of accereted income tax. As per amednded provisions, in case of cancellation of registration , where appeal before ITAT is not filed against the order of cancellation, accereted Income tax to be paid with in 14 days from the date of expiry of period of filing appeal.

However, where appeal has been filed but ITAT has confirmed the order of cancellation, accereted Income tax to be paid with in 14 days from the date of receipt of order of cancellation.

; or

(ii) it has adopted or undertaken modification of its objects which do not conform to the conditions of registration and it,—

(a) has not applied for fresh registration under section 12AA in the said previous year. Accereted Income tax to be paid with in 14 days from the end of previous year in which objects are modified[S.115TD(5)(ii)]; or

(b) has filed application for fresh registration under section 12AA but the said application has been rejected. Accereted Income tax to be paid with in 14 days from date of rejection [115TD(5)(iii)] However 115TD(5)(iii) was amended by the Parliament in Loksabha to extend the period of payment of accereted income tax. As per amednded provisions, in case of cancellation of registration , where appeal before ITAT is not filed against the order of rejection, accereted Income tax to be paid with in 14 days from the date of expiry of period of filing appeal.

However, where appeal has been filed but ITAT has confirmed the order of cancellation, accereted Income tax to be paid with in 14 days from the date of receipt of order of rejection.

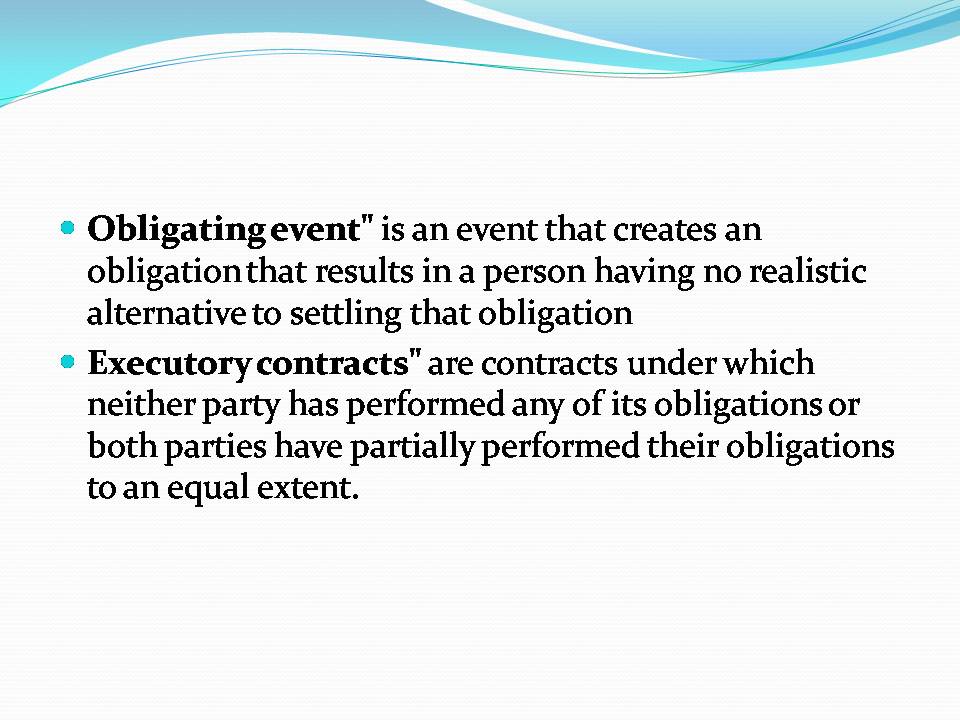

Comments: As per Section 12AA(3) and 12AA(4), registration of trust can be cancelled in following circumstances:

iii) income under rules enures for benefit of trustee etc or any part of income or property used applied for benefit of trustee

iv)Funds not invested as per 11(5).

Hence technical breaches like application of any part of income for benefit of trutee, violation of 11(5) etc.

CBDT has issued a Circular No. 21/2016 dated 27-05-2016, and has clarified that that the process for cancellation of registration is to be initiated strictly in accordance with section 12AA(3) and 12AA(4) after carefully examining the applicability of these provisions.

CBDT has also cautioned that since cancellation of registration of trust shall invite accereted income tax as per Finance Act 2016, authorities are, therefore, advised not to cancel the registration of a charitable institution granted u/s 12AA just because the proviso to section 2(15) comes into play

Here it may be noted that mere merger with trust registered u/s 12AA is not sufficient. It should also have similar objects. Dissimilar objects of trust registered u/s 12AA shall also attract accereted income tax . Further merger with institutions covered by 10(23C) but not registered u/s 12AA might also invite accereted income tax.

sub-clause (v) or sub-clause (vi) or sub-clause (via) of clause (23C) of section 10, within a period of twelve months from the end of the month in which the dissolution takes place Accereted Income tax as per S.115TD(5)(v) to be paid with in 14 days from the end of 12 month. The person to whom assets are transferred shall be liable to pay tax as assessee in default to the extent of assets received are capable of meeting liability as per S.115TF(2) and proviso to 115TF(2)

Provided that so much of the accreted income as is attributable to the following asset and liability, if any, related to such asset shall be ignored for the purposes of sub-section (1), namely:—

(i) any asset which is established to have been directly acquired by the trust or institution out of its income of the nature referred to in clause (1) of section 10;

(ii) any asset acquired by the trust or institution during the period beginning from the date of its creation or establishment and ending on the date from which the registration under section 12AA became effective, if the trust or institution has not been allowed any benefit of sections 11 and 12 during the said period:

Provided further that where due to the first proviso to sub-section (2) of section 12A, the benefit of sections 11 and 12 have been allowed to the trust or the institution in respect of any previous year or years beginning prior to the date from which the registration under section 12AA is effective, then, for the purposes of clause (ii) of the first proviso, the registration shall be deemed to have become effective from the first day of the earliest previous year:

Benefit of Additional depreciation @20% of actual cost u/s 32(1)(iia) which was earlier available to power sector concerns in generation or generation and distribution of power now also extended to power distribution or transmission concerns . Wef AY 2017-18

In Finance Bill following further provisions added by Loksabha while passing the bill

(3) The eligible assessee may exercise the option for taxation of income by way of royalty in respect of a patent developed and registered in India in accordance with the provisions of this section, in the prescribed manner, on or before the due date specified under sub-section (1) of section 139 for furnishing the return of income for the relevant previous year.

(4) Where an eligible assessee opts for taxation of income by way of royalty in respect of a patent developed and registered in India for any previous year in accordance with the provisions of this section and the assessee offers the income for taxation for any of the five assessment years relevant to the previous year succeeding the previous year not in accordance with the provisions of sub-section (1), then, theassessee shall not be eligible to claim the benefit of the provisions of this section for five assessment years subsequent to the assessment year relevant to the previous year in which such income has not been offered to tax in accordance with the provisions of sub-section (1).

[115BF(4) is similar to Section 44AD(4)]

are eligible for 100% deduction of profits and gains under newly introduced section 80IAC wef AY 2017-18 for any three consecutive assessment years out of five years beginning from the year in which the eligible start-up is incorporated.

Other conditions of not formed by splitting up or reconstruction of existing business; transfer of old machinery and applicability of 80IA (7) to 80IA(11) are also applicable

Note: What if deduction in first three years is claimed and fourth year turnover exceeds 25 crores ? Whether income shall be recomputed? Section is silent.

Conditions:

Amendments introduced in Finance Bill

As per bill introduced, the competent authority was required to approved as per prescribed guideline, however, in Finance Act, the requirement of approval with separate prescribed guidelines has been done away. Since approval for building plan is generally granted by local bodies, hence requirement of Competent authority being empowered by Central Government has also been done away at the time passing bill in Lok Sabha. Rather now competent authority means the authority empowered to approve the building plan by or under any law for the time being in force

| Min. plot area | 1000 sq mts=10763 sq ft |

| Max residential unit area | 30 sq mts i.e. 322.91 sq ft |

| Utilization of permissible Floor Area ratio | Min. 90% |

| Min. plot area | 2000 sq mts=21527 sq ft |

| Max residential unit area | 60 sq mts i.e. 645 .83sq ft |

| Utilization of permissible Floor Area ratio | Min. 80% |

Note : For Affordable Housing Project there is also a deducation u/s 35AD for capital expenditure @ 150% which has been brought down to 100% wef AY 2018-19

Enhanced deduction of Rs. 2 lacs for interest on housing loan on construction or acquisition for self occupied house is granted subject to condition that acquisition or construction is completed with in three year from the end of financial year in which the capital is borrowed. Limit of three years enhanced to five years wef AY 2017-18

Comments: If a person subscribes loan during 2011-12, he is required to complete construction till 31-03-2015, however, if construction is not completed till 31-03-2015 but in financial year 2015-16, the assessee is not entitled for deduction of enhanced amount of Rs. 2 lacs for AY 2016-17. However for AY 2017-18, the same assessee might become eligible for deduction of interest up to Rs. 2 lacs.

On the other hand, another assessee, who completes the construction in the year 2016-17 only, shall be entitled to enhanced deduction of Rs. 2 lacs from the very first year of completion.

So, a person who completes the house early also does not stand to gain.

iii) Additional Emoluments do not include:

In case of assessee,

Least of the Following deduction is allowed u/s 80GG:

iii) Rs. 2000 per month

Limit of Rs. 2000 pm enhanced to Rs. 5000 pm from AY 2017-18

When shares of private company are received by firm or company u/s 56(2)(viia) , transactions not regarded as transfers like receipt of shares in amalgamation or demerger are excluded, However there is no corresponding exception when shares are received by Individual / HUF u/s 56(2)(vii). Hence exception to this effect also incorporated in 56(2)(vii)

Comparative Positions of older and proposed provisions of 44AD(1) to 44AD(5) is reproduced below:

| 44AD(1) | (1) Notwithstanding anything to the contrary contained in sections 28to 43C, in the case of an eligible assessee engaged in an eligible business, a sum equal to eight per cent of the total turnover or gross receipts of the assessee in the previous year on account of such business or, as the case may be, a sum higher than the aforesaid sum claimed to have been earned by the eligible assessee, shall be deemed to be the profits and gains of such business chargeable to tax under the head “Profits and gains of business or profession”. | No Change |

| 44AD(2) | (2) Any deduction allowable under the provisions of sections 30 to 38 shall, for the purposes of sub-section (1), be deemed to have been already given full effect to and no further deduction under those sections shall be allowed | No Change |

| 44AD(2) Proviso | Provided that where the eligible assessee is a firm, the salary and interest paid to its partners shall be deducted from the income computed under sub-section (1) subject to the conditions and limits specified in clause (b) of section 40. | Omitted |

| 44AD(3) | The written down value of any asset of an eligible business shall be deemed to have been calculated as if the eligible assessee had claimed and had been actually allowed the deduction in respect of the depreciation for each of the relevant assessment years. | No Change |

| 44AD(4) | The provisions of Chapter XVII-C shall not apply to an eligible assessee in so far as they relate to the eligible business. | Where an eligible assessee declares profit for any previous year in accordance with the provisions of this section and

he declares profit for any of the five assessment years relevant to the previous year succeeding such previous year not in accordance with the provisions of sub-section (1), he shall not be eligible to claim the benefit of the provisions of this section for five assessment years subsequent to the assessment year relevant to the previous year in which the profit has not been declared in accordance with the provisions of sub-section (1) |

| 44AD(5) | Notwithstanding anything contained in the foregoing provisions of this section, an eligible assessee who claims that his profits and gains from the eligible business are lower than the profits and gains specified in sub-section (1) and whose total income exceeds the maximum amount which is not chargeable to income-tax, shall be required to keep and maintain such books of account and other documents as required under sub-section (2) of section 44AAand get them audited and furnish a report of such audit as required undersection 44AB. | Notwithstanding anything contained in the foregoing provisions of this section,

an eligible assessee to whom the provisions of sub-section (4) are applicable and whose total income exceeds the maximum amount which is not chargeable to income-tax , shall be required to keep and maintain such books of account and other documents as required under sub-section (2) of section 44AA and get them audited and furnish a report of such audit as required under section 44AB. |

Section 44AD(4) as proposed to be amended by Finance Bill 2016

Ø Where an eligible assessee declares profit for any previous year in accordance with the provisions of this section and

Ø he declares profit for any of the five assessment years relevant to the previous year succeeding such previous year not in accordance with the provisions of sub-section (1),

Ø he shall not be eligible to claim the benefit of the provisions of this section for five assessment years subsequent to the assessment year relevant to the

previous year in which the profit has not been declared in accordance with the provisions of sub-section (1)

Now let us analyse the benefits available u/s 44AD

Benefits u/s 44AD(1)

8% of total turnover or higher sum is deemed to be income of eligible business, overriding the provisions of section 28 to 43C [but not 44AA and 44AB].

Benefit u/s 44AD(2)

Deduction u/s 33 to 38 is deemed to have been allowed. Hence there is no actual benefit but rather benefit if any, is taken away in lieu of 8% or higher sum deemed to be income of the assessee

Benfit u/s 44AD(3)

WDV of business is calculated as if depreciation has been allowed

Hence benefit, if any is there in section 44AD(1) and not in any other provision. However section 44AD(1) does not talk about books or audit, which are separately dealt in 44AA and 44AB

Section 44AD(5) as proposed to be amended by Finance Bill 2016

Ø Notwithstanding anything contained in the foregoing provisions of this section,

Ø an eligible assessee to whom the provisions of sub-section (4) are applicable and whose total income exceeds the maximum amount which is not chargeable to income-tax ,

Ø shall be required to keep and maintain such books of account and other documents as required under sub-section (2) of section 44AA and

Ø get them audited and furnish a report of such audit as required under section 44AB.

Section 44AA(2)(iv)

Every assessee carrying on business shall

…………………………

Where the provisions of sub-section (4) of section 44AD are applicable in his case and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year

Keep and maintain such books of accounts and other documents as may enable the assessing officer to compute his total income in accordance with the provisions of this Act

Section 44AB(e)

Every person

carrying on the business shall, if the provisions of sub-section (4) of section 44AD are applicable in his case and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year

get his accounts of such previous audited……..

Hence S.44AA(2)(iv) and 44AB(e) are just corollary to what is said in 44AD(5)

Now the issue is when is section 44AD(4) applicable

Section 44AD(4) has two parts one is the applicability (or operative part )and other is substantive part. Section 44AD(5) is also speaks of consequences of applicability of 44AD(4)

Applicability (Or operative) part

Ø Where an eligible assessee declares profit for any previous year in accordance with the provisions of this section and

Ø he declares profit for any of the five assessment years relevant to the previous year succeeding such previous year not in accordance with the provisions of sub-section (1),

Consequence Part in 44AD(4)

Ø he shall not be eligible to claim the benefit of the provisions of this section for five assessment years subsequent to the assessment year relevant to the

previous year in which the profit has not been declared in accordance with the provisions of sub-section (1)

Implications

The assessee shall forego the benefit once the profit of six consecutive years is not shown at 8%, hence actual profit shall be computed for next five years.

This consequence shall also apply even if income is computed at lower than exemption limit and assessee can not reflect higher income to convert his undisclosed income into disclosed income

Consequence part in 44AD(5)

Eligible assessee to whom 44AD(4) applies and income is more than exemption limit

Ø shall be required to keep and maintain such books of account and other documents as required under sub-section (2) of section 44AA and

Ø get them audited and furnish a report of such audit as required under section 44AB.

E.g. Year 1 profit is 8% or higher

Year 2 profit is less than 8%

Then section 44AD(5) states that for Year 3 to Year 7, if income is more than exemption limit, the assessee shall have to get the accounts prepared and get the audit done.

Now there can be following propositions:

iii) If in year 3 to year 7, income is more than 8% and also higher than exemption limit, whether still maintenance of prescribed books and audit required where turnover is lesser than two crores?

If the answer is yes, because it is as per amended provision, it defies the logic of presumptive income scheme itself.

If answer is no, then it is obliteration of express provisions of the law

In the both the above situations, since 44AD(4) is not

applicable and as per 44AD(5) as well as 44AA(2)(iv) and 44AB(e), maintenance of books and audit is required only when 44AD(4) is applicable, books/ audit not required for Year 8 or Year 1 respectively in above propositions.

Although in such situation one might argue that books may be required to be maintained because of 44AA(2)(i)/(ii) but Memorandum explaining provisions of Finance Bill 2009 mentioned that “An assessee opting for the above scheme shall be exempted from maintenance of books of accounts related to such business as required under section 44AA of the Income-tax Act”

Another Interesting proposition of drafting 44AD(4) and 44AD(5) is that requirement of carrying out eligible business has also been dispensed with, while it is there in 44AD(5) in present form. Whether it is intentional or unintentional, only draftsmen know.

Retroactive application of Section 44AD(4) and 44AD(5)

The provisions have been amended wef AY 2017-18. However it is not clear that if, if assessee once covered by 44AD(1) has shown lesser than 8% income for period earlier that AY 2017-18, whether 44AD(4) and 44AD(5) shall become applicable wef AY 2017-18. It means that if operative part of 44AD(4) becomes applicable to the assessee for AY 2017-18, it might get covered by proposed provisions. Hence the amendment may have retroactive if not retrospective application.

Since section 44AD in present for came into existence wef AY 2011-12, let us take an example. Suppose for AY 2011-12, income was declared at 8% or higher sum but in any of five subsequent assessment year i.e. AY 2012-13 to AY 2016-17, income is declared lesser than 8%, then section 44AD benefit shall not apply for AY 2017-18 as per proposed amendment in 44AD(4).

Impact of not enhancing audit limit for business u/s 44AD

By not amending section 44AB(a) in the Finance Bill , the situation has been made more perplexing. This implies that if assessee’s turnover is between one crore and two crore he needs to get his accounts audited u/s 44AB(a) inspite of being covered by presumptive taxation u/s 44AD up to two crores.

Special Allowance of partners’ salary and interest to firm abolished ; Implications

Following proviso to 44AD(2) is proposed to be omitted wef AY 2017-18:

“Provided that where the eligible assessee is a firm, the salary and interest paid to its partners shall be deducted from the income computed under sub-section (1) subject to the conditions and limits specified in clause (b) of section 40.”

Implications

As per Supreme Court in Munjal Sales Corporation 298 ITR 298, interest to partner is covered by 36(1)(iii) and section 40(b) only places a restriction. Similarly salary to partner is covered by Section 37 and Section 40(b) only places restriction upon the same.

By Omissions of proviso to section 44AD(2) the provisions of 44AD(2) shall come into play which says that deductions u/s 30 to section 38 shall be deemed to have been given full effect . Therefore full effect shall be deemed to have been given effect to partners salary and interest covered respectively by 36(1)(iii) and section 37.

Hence if partnership deed provides for salary and interest to partners, while no deduction shall be allowable for presumptive taxation u/s 44AD, it might become taxable in the hands of partner u/s 28(v)

One school of thought is that fiction is not to be extended beyond the purpose for which it is created (Supreme Court in Bengal Immunity). Hence deeming fiction that full effect is deemed to have been given to deductions u/s 30 to 38 for presumptive taxation of firm can not be extended to tax interest and salary, deemed to have been allowed as deduction for firm, in the hands of the partner.

Another school of thought is that full effect must be given to the statutory fiction and it should be carried to its logical conclusion and to that end it would be proper and even necessary to assume all those facts on which alone the fiction can operate. By following this proposition, interest and salary shall become taxable in the hands of partner merely by virtue of provisions of partnership deed even though no separate deduction is allowed to the firm.

i.e AY 2018-19:

Examples of a few following assets with currents rates of depreciation that shall be affected are:

Comments: Memorandum Explaining provisions of finance bill have mentioned about this change, however, the Finance Act 2016 is silent on this change. Law in this regard may be framed in times to come

For following business deduction @ 150% was available by virtue of S. 35AD(1A) which has been omitted wef AY 2018-19,

Thus only 100% deduction shall be available for above Businesses

Note : For affordable housing 100% profit linked deduction also introduced by incorporating S. 80-IBA wef AY 2017-18

allowed as deduction to be carried forward only if return is filed in time. Necessary amendments made in S.80 and Section 139(3)

At present u/s 36(1)(viia) , following deduction on account of provisioning for bad and doubtful debts is allowed:

| a) | Scheduled Banks (not being foreign banks) , non schedules banks, co-operative banks (Other than PACS, Agri cultural and Rural developments banks)

Optional Allowance for Scheduled and non Scheduled banks for assets classified by RBI as doubtful or loss assets in accordance with guidelines |

7.5% of Income + 10% of Agg. Avg. Advances made by Rural branches

Max. 5% of such assets shown in the books of accounts of the bank on last day of previous year |

| b) | Foreign Banks | 5% of Income |

| c) | Public Financial Institutions, State Financial Corporation or State Industrial Investment Corporation | 5% of Income |

| Note : Income is computed before allowing deduction under Chapter VI-A and deduction under 36(1)(viia) | ||

Since NBFCs are also engaged in lending to different sector similar deduction being allowed to NBFCs also up to 5% of Income wef AY 2017-18.

As per section 206AA which has overriding impact on the all other provisions of the Act, in case of failure to furnish PAN to the deductor, highest of the following rates shall apply:

In case of non resident, as per section 115A(b), rate of 10% is applicable for royalty and fee for technical services. However, if non resident is not having PAN, tax shall be deducted @ 20%.

Section 206AA(7) which provides relief to non residents from applicaton of 206AA in respect of TDS on long term infrastructure bonds has been extended to all other payments subject to complying prescribed conditions.

Comments Here it may be noted that as per ITAT Pune Bench in Serum Institute pronounced on 30-03-2015, even in the absence of PAN payer not required to deduct TDS at 20% if case covered by DTAA.

As per Section 115BBE inserted wef AY 2013-14, tax rate of 30% is to applied to income chargeable to tax u/s 68,69,69A,B,C,D Also no deduction for any expenditure or allowance is allowed in respect of income assessed under these sections.

Memorandum explaining provisions of Finance Bill says that there is uncertainty on the issue of set-off of losses against income referred in section 115BBE of the Act. The matter has been carried to judicial forums and courts in some cases has taken a view that losses shall not be allowed to be set-off against income referred to in section 115BBE. However, the current language of section 115BBE of the Act does not convey the desired intention and as a result the matter is litigated. In order to avoid unnecessary litigation, it is proposed to amend the provisions of the sub-section (2) of section 115BBE to expressly provide that no set off of any loss shall be allowable in respect of income under the sections 68 or section 69 or section 69A or section 69B or section 69C or section 69D. This amendment shall have effect from AY 2017-18.

Comments: Whether this leads to argument that Punjab and Haryana High Court ruling may not be applied for period preceding AY 2017-18 or amendment is clarificatory in nature. However depreciation and Unabsorbed depreciation already stands covered by word “allowance wef AY 2013-14”

It was held by ITAT Delhi in Satya Sheel Khosla 63 taxmann.com 293 quoting para 28 on page 692 of Kanga and Palkhiwala that u/s 28(va) consideration received for restrictive covenants is taxable in case of business but not taxable in case of profession . Hence consideration received for restrictive covenants in profession also being made taxable wef AY 2017-18.

It was held by ITAT Chennai in K. Prem Raj 41 taxmann.com 81 that sale of goodwill of profession would not as such come within ambit of provisions of section 55(2)(a); same is not taxable as LTCG. Hence section 55 (2)(a) being amended to provide that cost of acquisition of self generated goodwill of profession shall be NIL, so that it also becomes taxable under Capital gain wef AY 2017-18 and supreme court decision in BC SreeNiwas Shetty no longer operates for self generated goodwill of profession.

Under the existing provisions contained in Section 50C, in case of transfer of a capital asset being land or building on both, the value adopted or assessed by the stamp valuation authority for the purpose of payment of stamp duty shall be taken as the full value of consideration for the purposes of computation of capital gains.

The Income Tax Simplification Committee (Easwar Committee) has in its first report, pointed out that this provision does not provide any relief where the seller has entered into an agreement to sell the property much before the actual date of transfer of the immovable property and the sale consideration is fixed in such agreement, whereas similar provision exists in section 43CA of the Act i.e. when an immovable property is sold as a stock-in-trade.

It is proposed to amend the provisions of section 50C so as to provide that where the date of the agreement fixing the amount of consideration for the transfer of immovable property and the date of registration are not the same, the stamp duty value on the date of the agreement may be taken for the purposes of computing the full value of consideration.

It is further proposed to provide that this provision shall apply only in a case where the amount of consideration referred to therein, or a part thereof, has been paid by way of an account payee cheque or account payee bank draft or use of electronic clearing system through a bank account, on or before the date of the agreement for the transfer of such immovable property.

As per section 2(42A) of the Income-tax Act, any capital asset held by the taxpayer for a period of not more than 36 months immediately preceding the date of its transfer is treated as short-term capital asset.

The aforesaid period of 36 months is treated as 12 months in case of shares held in a company. However, an amendment was made by Finance Act (No. 2) Act, 2014 to provide that the said period of 12 months won’t be applicable in respect of shares not listed in recognized stock exchange. Hence, with effect from 01.04.2015, unlisted share is treated as short-term capital asset if it is held for not more than 36 months immediately preceding the date of its transfer.

The Finance Bill, 2016 as passed by the Lok Sabha inserted a new clause to provide that the period of 36 months would be substituted with period of 24 months in case of unlisted shares. In other words, unlisted shares of company would be treated as short-term capital asset if it is held for a period of 24 months or less immediately preceding the date of its transfer. This change is effective from AY 2017-18

By amending sixth proviso to S.139(1), return of filing made compulsory even if income of the assessee without claiming exemption exceeds maximum amount not chargeable to tax. However no such requirement for long term capital loss covered by 10(38).

Finance Act 2013 wef 01-06-2013 had inserted clause (aa) in section 139(9) to provide that a return of income shall be regarded as defective unless the tax together with interest, if any, payable in accordance with the provisions of section 140A, has been paid on or before the date of furnishing of the return

Now clause(aa) has been removed, Hence return shall not be defective for non payment of tax and interest on or before date of furnishing return of income

Current Provisions

(4) Any person who has not furnished a return within the time allowed to him under sub-section (1), or within the time allowed under a notice issued under sub-section (1) of section 142, may furnish the return for any previous year at any time before the expiry of one year from the end of the relevant assessment year or before the completion of the assessment, whichever is earlier

Amended Provisions

“(4) Any person who has not furnished a return within the time allowed to him under sub-section (1), may furnish the return for any previous year at any time before the end of the relevant assessment year or before the completion of the assessment, whichever is earlier

Implications: 1. Return not filed in response to notice u/s 142 can not be filed belatedly and to be filed with in time allowed u/s 142 or such further time as may be allowed by AO from time to time. [As per section 14 of General Clauses Act]

Current Provisions

If any person, having furnished a return under sub-section (1), or in pursuance of a notice issued under sub-section (1) of section 142, discovers any omission or any wrong statement therein, he may furnish a revised return at any time before the expiry of one year from the end of the relevant assessment year or before the completion of the assessment, whichever is earlier

Amended Provisions

If any person, having furnished a return under sub-section (1) or sub-section (4), discovers any omission or any wrong statement therein, he may furnish a revised return at any time before the expiry of one year from the end of the relevant assessment year or before the completion of the assessment, whichever is earlier

Implications

Belated return u/s 139(4) can also be rectified. Belated return u/s 142(1) can not be rectified.

However memorandum explaining provisions of Finance bill still mentions about return furnished in response to notice u/s 142 which is inconsistent with express amendment.

As per section 143(1)(a) while processing return the total income or loss shall be computed after making the adjustments for

(i) any arithmetical error in the return or